Paying bills on time is one of the most important parts of everyday money management.

Rent, mortgage, electricity, gas, water, internet, mobile phone, insurance, credit cards, subscriptions, loan payments, school fees, business software, and utility bills can become difficult to manage when they are spread across different due dates.

This is why online bill pay and automatic payments are useful.

A good bank account can help users schedule bills, create recurring payments, receive reminders, avoid late fees, track outgoing money, manage subscriptions, and protect accounts from suspicious activity.

But online bill pay is not only about convenience.

It also needs safety.

Automatic payments can prevent missed bills, but they can also create problems if users forget about subscriptions, keep too little balance in the account, authorize unreliable companies, or fail to cancel recurring charges.

The best banks for online bill pay and automatic payments should offer:

- Easy bill payment setup

- One-time and recurring payments

- Bill reminders

- eBills, where available

- Mobile app access

- Payment status tracking

- Strong account alerts

- Debit card controls

- Overdraft protection choices

- Clear fees

- Good customer support

- Secure login

- FDIC or NCUA coverage

- Fast transfer tools

- Easy cancellation or editing of scheduled payments

This guide compares the best banks and digital banking options for online bill pay and automatic payments, explains how autopay works, and gives safety tips to avoid missed bills, overdrafts, scams, and unwanted recurring charges.

Important Disclaimer

This article is for general informational purposes only. It is not banking, legal, tax, investment, accounting, cybersecurity, payment, or professional advice.

Online bill pay features, automatic payment rules, ACH policies, account fees, overdraft rules, payment timing, biller availability, cancellation rights, dispute protections, transfer limits, and bank features can change. Always verify details directly with the bank, biller, payment provider, or qualified professional before setting up or canceling automatic payments.

What Is Online Bill Pay?

Online bill pay is a banking feature that lets users pay bills through a bank website or mobile app.

Instead of visiting each biller’s website separately, writing checks, or mailing payments, users can pay bills from one place.

Online bill pay may allow users to:

- Pay utility bills

- Pay rent

- Pay mortgage

- Pay credit cards

- Pay insurance

- Pay phone bills

- Pay internet bills

- Pay medical bills

- Pay loan bills

- Pay subscriptions

- Pay individuals, depending on bank rules

- Schedule future payments

- Create recurring payments

- Receive bill reminders

- View payment history

- Track payment status

Some bill payments are sent electronically. Others may be sent by paper check if the biller does not accept electronic payments through the bank’s system.

What Are Automatic Payments?

Automatic payments are recurring payments that happen on a schedule.

They may be set up through:

- Your bank’s online bill pay

- A biller’s website

- ACH authorization from your bank account

- Debit card recurring payment

- Credit card recurring payment

- Payment app

- Subscription platform

Automatic payments can be fixed or variable.

A fixed automatic payment is the same amount each time.

Examples:

- Rent

- Loan payment

- Insurance premium

- Subscription fee

- Gym membership

A variable automatic payment changes each time.

Examples:

- Electricity bill

- Gas bill

- Water bill

- Credit card statement balance

- Mobile phone bill

- Usage-based software bill

Autopay can be helpful, but users should monitor it carefully.

Online Bill Pay vs Autopay

Online bill pay and autopay are similar, but not always the same.

Online Bill Pay

Usually controlled through your bank.

Best for:

- Scheduling bills manually

- Paying from one dashboard

- Creating recurring bank payments

- Tracking payment history

- Avoiding multiple biller logins

- Paying companies that accept bill pay

Autopay

Usually controlled through the biller or payment provider.

Best for:

- Regular recurring payments

- Subscriptions

- Credit card minimum payments

- Loan payments

- Utility bills

- Insurance premiums

Main Difference

With bank bill pay, you often push money from your bank to the biller.

With autopay, the biller may pull money from your bank account or card after you authorize it.

Both can be useful, but autopay requires more careful monitoring.

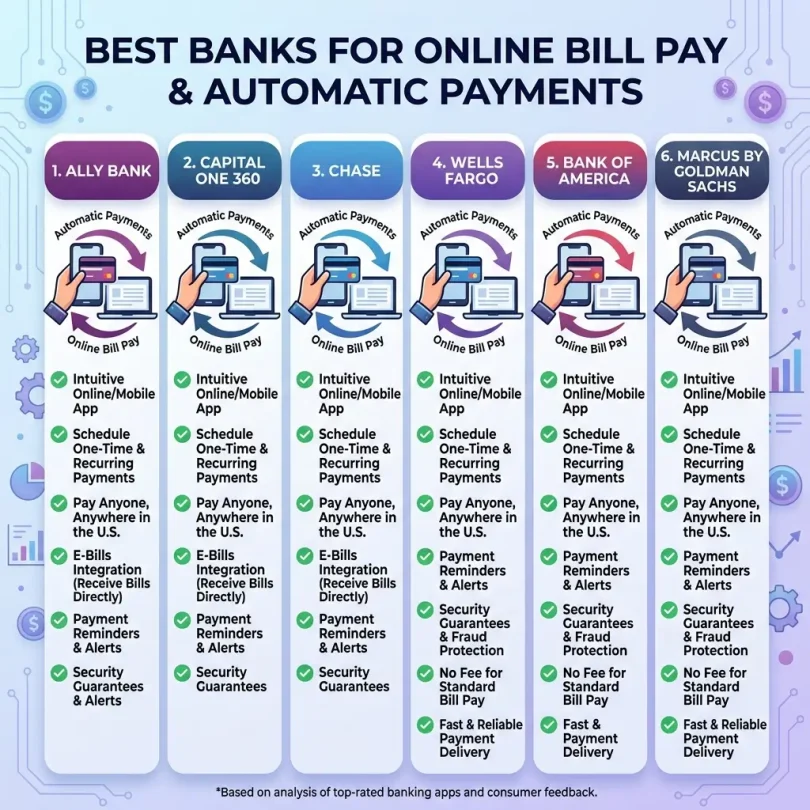

Best Banks for Online Bill Pay and Automatic Payments

Below are strong options to compare for online bill pay, automatic payments, account alerts, and mobile banking convenience.

1. Chase

Best for: Full-service bill pay and large-bank account management

Good for: Checking users, credit card users, mortgage users, families, businesses

Main strength: Strong online bill pay tools with recurring payment setup

Chase is one of the strongest options for users who want online bill pay from a large bank.

Chase online bill pay allows users to pay bills such as utilities, services, and other payees, set up recurring online payments, sign up for eBills, and track payment status.

Key Features

- Online bill pay

- Recurring payments

- eBills, where available

- Bill reminders

- Payment tracking

- Mobile app access

- Zelle, where available

- Transfers

- Credit card payments

- Mortgage and loan access, depending on account

- Debit card controls

- Account alerts

- Branch support

- Large ATM network

- Business banking options

Why Chase Is Good

Chase is useful for people who want everything in one banking relationship.

If you have Chase checking, credit cards, mortgage, auto loan, business account, or savings, the app can make account management easier.

Chase is also strong for people who want both digital tools and branch support.

Best Fit

Chase may fit:

- Large-bank users

- Families

- Bill pay users

- Credit card users

- Mortgage users

- Small businesses

- Branch users

- Users who want payment tracking

Possible Downsides

Some Chase checking accounts may have monthly fees unless waiver requirements are met. Users should compare account fee rules before opening.

2. Bank of America

Best for: Online bill pay, recurring payments and mobile bill management

Good for: Existing customers, families, large-bank users, branch users

Main strength: Strong bill pay feature inside online and mobile banking

Bank of America offers online bill pay through online banking and the mobile app. Users can set up one-time payments, future payments, or recurring payments from eligible accounts.

Bank of America bill pay is useful for users who want to manage multiple bills from one bank dashboard.

Key Features

- Online bill pay

- Mobile bill pay

- One-time payments

- Future-dated payments

- Recurring payments

- eBills, where available

- Payment reminders

- Payment history

- Transfers

- Zelle, where available

- Debit card controls

- Erica virtual assistant

- Branch and ATM access

- Business banking options

Why Bank of America Is Good

Bank of America is useful for people who want a large-bank app with bill pay, reminders, card tools, and branch support.

It can work well for households managing many bills.

Best Fit

Bank of America may fit:

- Existing Bank of America customers

- Families

- Branch users

- Credit card users

- Bill pay users

- People wanting recurring payments

- Large-bank customers

- Small business users

Possible Downsides

Monthly maintenance fees may apply on some checking accounts unless requirements are met. Users should check account terms.

3. Capital One

Best for: Fee-friendly checking and simple bill pay

Good for: Online checking users, no-monthly-fee users, mobile app users

Main strength: Digital banking with bill pay and account alerts

Capital One offers online bill pay features that can help users schedule one-time or recurring payments from eligible accounts.

Capital One is also popular because many 360 banking products focus on low fees and strong mobile access.

Key Features

- Online bill pay

- One-time payments

- Recurring payments

- Checking and savings

- Debit card

- Mobile app

- Account alerts

- Card lock

- Transfers

- ATM access

- Large-bank brand

- No monthly fees on many 360 products

- Branch or café access in some areas

Why Capital One Is Good

Capital One can be a strong option for users who want online bill pay without complicated account fees.

It is especially good for users who want a simple app, checking, savings, and card controls.

Best Fit

Capital One may fit:

- Online checking users

- No-monthly-fee seekers

- Mobile banking users

- Families

- Bill pay users

- Card control users

- Beginners

Possible Downsides

Branch access depends on location, and some bill pay features may depend on account type.

4. Ally Bank

Best for: Online-only bill pay and savings organization

Good for: Online banking users, no-branch users, savings users

Main strength: Strong online banking ecosystem with checking and savings tools

Ally Bank is a popular online bank with checking-style and savings products.

It can be useful for users who want online bill pay, transfers, savings buckets, debit card access, and mobile banking without branch visits.

Key Features

- Online bill pay

- Checking-style Spending Account

- Online savings

- Debit card

- Mobile check deposit

- Transfers

- ATM access

- Account alerts

- Savings buckets

- Automatic savings tools

- No branch requirement

- FDIC-insured bank

Why Ally Is Good

Ally is useful for people who want a fully online bank that can handle bills, transfers, savings goals, and everyday spending.

It works well for users who want to keep bill money separate from emergency savings or savings buckets.

Best Fit

Ally may fit:

- Online banking users

- Emergency fund users

- Bill pay users

- Savings bucket users

- People avoiding branch banking

- Mobile banking users

Possible Downsides

Ally does not have physical branches. Cash deposits can be difficult.

5. Discover Bank

Best for: No-fee online banking and simple bill management

Good for: Debit card users, savings users, online checking users

Main strength: Simple online account experience

Discover Bank offers online checking and savings products that can work well for users who want simple digital banking.

Discover is known for no monthly fees on many banking products and cashback debit features on eligible debit purchases.

Key Features

- Online checking

- Online savings

- Bill pay

- Debit card

- Mobile banking

- Mobile check deposit

- Account alerts

- Transfers

- Card lock

- No monthly fees on many accounts

- FDIC-insured bank

Why Discover Is Good

Discover can be a practical option for people who want simple online checking, debit card access, and bill pay tools without a monthly maintenance fee.

Best Fit

Discover may fit:

- Online checking users

- Debit card users

- Bill pay users

- No-fee account seekers

- Savings users

- Mobile app users

Possible Downsides

Discover may not be ideal for users who need branch access or frequent cash deposits.

6. Wells Fargo

Best for: Traditional bank bill pay with branch support

Good for: Branch users, households, existing Wells Fargo customers

Main strength: Bill pay plus large physical banking network

Wells Fargo offers online and mobile banking with bill pay, transfers, account alerts, card controls, and branch access.

It can be useful for users who prefer a traditional bank but still want digital bill payment tools.

Key Features

- Online bill pay

- Mobile banking

- Checking and savings

- Credit card access

- Transfers

- Zelle, where available

- Account alerts

- Debit card controls

- Branch access

- ATM access

- Business banking options

- Customer support

Why Wells Fargo Is Good

Wells Fargo may work for users who want branch support, online bill pay, and a traditional bank account.

It can also be useful for households with multiple Wells Fargo products.

Best Fit

Wells Fargo may fit:

- Existing customers

- Branch users

- Families

- Bill pay users

- Traditional bank users

- Small business owners

- People wanting in-person support

Possible Downsides

Account fees and waiver rules should be reviewed carefully. Some users may prefer online banks with fewer fees.

7. U.S. Bank

Best for: Digital bill pay with traditional bank support

Good for: Existing customers, branch users, online bill pay users

Main strength: Online payments and account management

U.S. Bank offers online banking and mobile banking features for bill payments, transfers, alerts, card management, and account tracking.

It can be a good option for users who want online bill pay from a bank with branch support in many areas.

Key Features

- Online bill pay

- Mobile bill pay

- Checking and savings

- Account alerts

- Transfers

- Zelle, where available

- Card controls

- Mobile check deposit

- ATM access

- Branch access

- Credit card and loan account management

Why U.S. Bank Is Good

U.S. Bank can be useful for people who want both online payment tools and traditional bank services.

Best Fit

U.S. Bank may fit:

- Existing U.S. Bank customers

- Branch users

- Bill pay users

- Families

- Credit card users

- Traditional bank customers

Possible Downsides

Monthly fees may apply to some accounts unless requirements are met. Users should compare fee schedules.

8. Charles Schwab Bank

Best for: Travelers and users who want checking with strong ATM benefits

Good for: Bill pay users, travelers, brokerage customers

Main strength: Checking account with bill pay and ATM flexibility

Schwab Bank Investor Checking is popular with travelers and users who want online checking connected to a brokerage relationship.

It supports online banking features and bill pay while also offering strong ATM-related benefits.

Key Features

- Online bill pay

- Checking account

- Debit card

- ATM fee rebates

- Online transfers

- Mobile banking

- Mobile check deposit

- No monthly service fee

- No account minimum

- Linked brokerage relationship

- FDIC-insured bank checking account

Why Schwab Is Good

Schwab can be useful for users who travel often and want a checking account that can still handle bill payments.

Best Fit

Schwab may fit:

- Travelers

- ATM users

- Bill pay users

- Brokerage customers

- Online banking users

- People who want fee-friendly checking

Possible Downsides

The linked brokerage account setup may not be ideal for users who only want simple checking.

9. Alliant Credit Union

Best for: Online credit union bill pay

Good for: Credit union users, checking users, savings users

Main strength: Credit union banking with online bill pay tools

Alliant Credit Union offers online checking and savings with digital banking tools.

It can be a good option for users who prefer credit unions but still want online bill payment and mobile banking.

Key Features

- Online bill pay

- Checking account

- Savings account

- Debit card

- Mobile banking

- Mobile check deposit

- ATM access

- Account alerts

- Online transfers

- NCUA-insured credit union

- Membership requirement

Why Alliant Is Good

Alliant is useful for users who want credit union-style banking with online access.

It can work well for everyday bills, debit card use, and savings management.

Best Fit

Alliant may fit:

- Credit union users

- Online banking users

- Bill pay users

- Checking users

- Savings users

- ATM users

- People comfortable with membership requirements

Possible Downsides

Membership requirements apply. Users should review eligibility before applying.

10. Bluevine Business Checking

Best for: Business bill pay and vendor payments

Good for: Small businesses, freelancers, agencies, consultants

Main strength: Business checking with bill pay and payment tools

Bluevine Business Checking is a strong option for small businesses that need to pay vendors, contractors, software bills, utilities, suppliers, and recurring business expenses.

It is especially useful for businesses that want online business checking, bill pay, ACH transfers, sub-accounts, and invoicing tools.

Key Features

- Business checking

- Bill pay

- ACH transfers

- Vendor payments

- Business debit card

- Sub-accounts

- Invoicing

- Mobile banking

- Accounting integrations

- No monthly fee on standard plan

- APY opportunity on eligible balances

- FDIC coverage through partner bank and program banks

Why Bluevine Is Good

Bluevine is useful for freelancers and small businesses that need organized online payments.

It can help separate taxes, payroll, operating expenses, and vendor payments from personal money.

Best Fit

Bluevine may fit:

- Freelancers

- Consultants

- Agencies

- Online businesses

- Small business owners

- Vendor payment users

- Businesses that need ACH payments

- Businesses wanting sub-accounts

Possible Downsides

Bluevine is mainly for businesses, not personal household bills. Users should review ACH, wire, deposit, and APY requirements.

Quick Comparison Table

| Bank or Provider | Best For | Main Strength | Best User Type |

|---|---|---|---|

| Chase | Full-service bill pay | Recurring payments and eBills | Large-bank users |

| Bank of America | Mobile bill management | One-time, future and recurring payments | Families |

| Capital One | Fee-friendly bill pay | Simple app and no-fee account options | Online checking users |

| Ally Bank | Online-only bill pay | Savings tools and online checking | Digital users |

| Discover Bank | Simple no-fee banking | Checking, bill pay and debit card tools | No-fee users |

| Wells Fargo | Branch plus bill pay | Traditional bank support | Branch users |

| U.S. Bank | Traditional digital banking | Online bill pay and card tools | Existing customers |

| Schwab Bank | Travelers | Bill pay plus ATM benefits | Travelers |

| Alliant Credit Union | Credit union bill pay | NCUA-insured online banking | Credit union users |

| Bluevine | Business payments | Vendor payments and ACH tools | Small businesses |

What Features Matter for Online Bill Pay?

1. One-Time Payments

A good bank should let you pay a bill one time without creating a recurring schedule.

Useful for:

- Medical bills

- Repairs

- Occasional services

- One-time invoices

- School fees

- Annual memberships

2. Recurring Payments

Recurring payments are useful for bills that repeat.

Examples:

- Rent

- Mortgage

- Insurance

- Internet

- Phone

- Utilities

- Loan payments

- Subscriptions

- Business software

3. eBills

eBills allow some bills to appear inside online banking.

They can help users:

- View amount due

- See due date

- Set reminders

- Pay from bank dashboard

- Track bill history

4. Bill Reminders

Bill reminders help prevent late fees.

Look for:

- Due date reminders

- Email reminders

- Push notifications

- Text alerts

- Calendar-style bill view

- Payment confirmation alerts

5. Payment Tracking

A good bill pay system should show:

- Scheduled payments

- Processing status

- Delivered payments

- Canceled payments

- Payment history

- Confirmation numbers

6. Mobile Access

Users should be able to schedule and manage bills from a phone.

7. Automatic Payment Editing

Users should be able to edit or cancel scheduled payments easily.

8. Security Alerts

Bill pay should connect with alerts for large transfers, new payees, and account changes.

9. Payee Management

Users should be able to add, edit, and remove payees safely.

10. Business Payment Tools

Small businesses may need:

- Vendor payments

- ACH payments

- Approval workflows

- Accounting exports

- Multiple users

- Payment records

- Contractor payments

Autopay From Bank Account vs Debit Card vs Credit Card

Bank Account Autopay

Best for:

- Utilities

- Mortgage

- Rent

- Insurance

- Loan payments

- Credit card payments

Pros:

- Direct payment from checking

- Often accepted by billers

- Useful for large bills

- May avoid card processing fees

Cons:

- Can cause overdraft if balance is low

- Biller may pull money automatically

- Cancellation may require contacting biller

- Less card-level dispute protection than some card payments

Debit Card Autopay

Best for:

- Subscriptions

- Phone bills

- App services

- Smaller recurring charges

Pros:

- Easy setup

- Card lock may help

- Can replace card if compromised

- Good for smaller bills

Cons:

- Card expiration can break payments

- Fraud risk if card details leak

- Disputes may take time

Credit Card Autopay

Best for:

- Subscriptions

- Utilities that accept cards without extra fee

- Travel services

- Software

- Streaming

- Business expenses

Pros:

- Better rewards potential

- Easier to track subscriptions

- Can avoid bank-account exposure

- Card replacement can stop some unwanted charges

- Strong dispute tools in many cases

Cons:

- Interest risk if card balance is not paid

- Some billers charge card fees

- Overspending risk

- Autopay failures if card expires

Best Bills to Put on Autopay

Autopay is best for stable, trusted bills.

Good autopay candidates:

- Mortgage

- Rent, if trusted system

- Insurance premiums

- Phone bill

- Internet bill

- Streaming subscriptions

- Software subscriptions

- Credit card minimum payment

- Student loan payment

- Car payment

- Utilities, if monitored

- Business software

- Cloud hosting

- Domain renewals

Be careful with variable bills if you do not monitor balances.

Bills to Monitor Closely Before Autopay

Some bills can change suddenly.

Monitor:

- Electricity

- Gas

- Water

- Credit card full balance

- Medical bills

- Usage-based software

- Cloud hosting

- International phone charges

- Payment plans with variable fees

- Subscriptions after free trial

For variable bills, set alerts before payment date.

Autopay Safety Tips

1. Keep a Bill Calendar

Even with autopay, keep a calendar of due dates.

Include:

- Biller name

- Payment date

- Payment amount

- Payment method

- Account used

- Cancellation link

- Customer support number

2. Use a Dedicated Bills Account

A separate checking account for bills can help.

Example:

- Main checking for income

- Bills checking for autopay

- Savings for emergency fund

- Separate business account

Move only the amount needed for bills into the bills account.

3. Turn On Low Balance Alerts

Low balance alerts can prevent overdrafts and failed payments.

4. Set Payment Alerts

Turn on alerts for:

- Payment scheduled

- Payment processed

- Large debit

- New payee added

- Failed payment

- Low balance

- Overdraft risk

5. Review Bills Monthly

Even automatic payments should be reviewed.

Check for:

- Price increases

- Duplicate charges

- Canceled services still billing

- Trial conversions

- Unknown subscriptions

- Billing errors

6. Avoid Autopay With Untrusted Companies

Do not give bank account authorization to companies you do not trust.

7. Use Credit Card for Risky Subscriptions

For subscriptions and trial offers, a credit card may be safer than direct bank debit, if you pay the card in full.

8. Keep Proof of Cancellation

Save:

- Cancellation confirmation

- Email receipts

- Chat screenshots

- Confirmation numbers

- Terms page

- Date canceled

9. Know How to Stop Automatic Payments

Users should understand how to revoke authorization and contact the bank if needed.

10. Check After Canceling

After canceling a service, check the next statement to make sure charges stopped.

How to Stop Automatic Payments

If you want to stop automatic debits from your bank account, start by contacting the company and taking away permission to withdraw money.

Then follow up in writing.

You can also contact your bank or credit union and ask how to stop future payments.

If a company keeps taking money after you revoke authorization, report it to your bank quickly.

Keep records of:

- Date you canceled

- Person you spoke with

- Confirmation number

- Email confirmation

- Screenshots

- Bank messages

- Any future charges

Common Online Bill Pay Mistakes

Mistake 1: Assuming Autopay Means No Monitoring

Autopay still needs monthly review.

Mistake 2: Forgetting Free Trials

Many people forget trial dates and get charged.

Mistake 3: Using the Wrong Account

A payment from the wrong account can cause overdraft or failed payment.

Mistake 4: Not Updating Expired Cards

Card-based autopay can fail when a card expires.

Mistake 5: Paying From Low-Balance Checking

Keep enough cushion in the bill-pay account.

Mistake 6: Not Saving Confirmation Numbers

Proof matters when a payment is missing.

Mistake 7: Trusting Every Bill Email

Fake bill emails are common. Open the app or official website directly.

Mistake 8: Not Removing Old Payees

Old payees can create confusion and risk.

Mistake 9: Paying Bills Too Late

Schedule payments early enough to process.

Mistake 10: Not Checking Paper Check Delivery

Some bank bill pay systems may send paper checks if electronic payment is unavailable. Allow extra time.

Online Bill Pay Security Tips

Use Strong Passwords

Use a unique password for your bank account.

Enable Two-Factor Authentication

Turn on 2FA, passkeys, or stronger login protection where available.

Protect Your Email

Your email receives bill reminders and bank alerts.

Verify New Payees

Before sending money, confirm payee details.

Avoid Clicking Bill Links

Fake bill links can steal login details.

Open the bank app or biller site directly.

Turn On Alerts

Alerts help detect suspicious activity.

Review Payment History

Check bill pay history monthly.

Remove Old Payees

Delete payees you no longer use.

Watch for Fake Invoices

Small businesses should verify vendor payment details.

Use Secure Networks

Avoid setting up bill payments on public Wi-Fi.

Online Bill Pay for Small Businesses

Small businesses need stronger controls.

Business bill pay may include:

- Vendor payments

- Contractor payments

- Software subscriptions

- Rent

- Utilities

- Insurance

- Supplier invoices

- Hosting bills

- Domain renewals

- Payroll-related payments

- Tax payments

- Loan payments

Business owners should use:

- Separate business account

- Approval rules

- Bookkeeper access

- Two-person review for large payments

- Vendor verification

- ACH controls

- Payment records

- Accounting integration

- Monthly reconciliation

Bluevine, Chase Business, Bank of America Business, U.S. Bank Business, Relay, Mercury, and other business-focused accounts may be useful depending on the company’s needs.

Online Bill Pay for Families

Families can use online bill pay to manage household expenses.

Useful setup:

- Shared bill calendar

- Dedicated bills account

- Automatic payments for fixed bills

- Manual review for variable bills

- Alerts for large payments

- Monthly subscription review

- Emergency fund in separate savings

This helps reduce missed payments and surprises.

Online Bill Pay for Freelancers

Freelancers can use online bill pay for:

- Internet

- Phone

- Software subscriptions

- Hosting

- Domains

- Contractor payments

- Taxes

- Insurance

- Coworking space

- Equipment financing

- Business credit card payments

Freelancers should separate business bills from personal bills.

Use a business account where appropriate.

Checklist Before Choosing a Bank for Bill Pay

Before choosing a bank, ask:

- Does the bank offer online bill pay?

- Can I schedule future payments?

- Can I create recurring payments?

- Are eBills available?

- Are reminders available?

- Can I track payment status?

- Can I cancel scheduled payments easily?

- Are there fees for bill pay?

- Are payments sent electronically or by paper check?

- How long do payments take?

- Does the app support mobile bill pay?

- Can I set alerts?

- Can I lock my debit card?

- Is 2FA available?

- Are there overdraft fees?

- Can I keep a separate bills account?

- Is customer support reliable?

- Is deposit insurance clear?

- Can business users add approvals?

- Are payment records easy to download?

Final Verdict: What Are the Best Banks for Online Bill Pay?

The best bank for online bill pay depends on your needs.

For most users:

- Best full-service bill pay: Chase

- Best mobile bill management: Bank of America

- Best fee-friendly bill pay: Capital One

- Best online-only bill pay: Ally Bank

- Best simple no-fee online banking: Discover Bank

- Best traditional bank with branch support: Wells Fargo

- Best traditional digital banking option: U.S. Bank

- Best for travelers: Charles Schwab Bank

- Best credit union option: Alliant Credit Union

- Best business bill pay: Bluevine Business Checking

If you want a large bank with strong bill pay, compare Chase and Bank of America. If you want fewer fees, compare Capital One, Ally, Discover, Schwab, and Alliant. If you run a business, compare Bluevine, Chase Business, Bank of America Business, Relay, Mercury, and U.S. Bank Business.

The best bill pay account is not only the one that pays bills. It should help you avoid late fees, track payments, manage cash flow, protect your account, and cancel or edit payments without stress.

FAQs About Online Bill Pay and Automatic Payments

What is online bill pay?

Online bill pay is a bank feature that lets users pay bills through a bank website or mobile app. Users can often schedule one-time, future, or recurring payments.

What is autopay?

Autopay is an automatic payment that repeats on a schedule. It may be set up through a bank, biller, card, ACH authorization, or payment app.

Which bank is best for online bill pay?

Chase, Bank of America, Capital One, Ally, Discover, Wells Fargo, U.S. Bank, Schwab, Alliant, and Bluevine are strong options depending on user needs.

Is online bill pay safe?

Online bill pay can be safe when used through trusted banks, strong passwords, two-factor authentication, alerts, and careful payee verification.

Is autopay safe?

Autopay can be safe for trusted billers, but users should monitor accounts, keep enough balance, and review charges regularly.

What is the difference between bill pay and autopay?

Bill pay is usually controlled through your bank. Autopay is often controlled by the biller, which may pull money from your bank account or card.

Can I stop automatic payments from my bank account?

Yes. You can contact the company to revoke permission and follow up in writing. You can also contact your bank or credit union for help stopping future payments.

Should I use a bank account or credit card for autopay?

Bank account autopay is useful for major bills. Credit card autopay may be better for subscriptions if you pay the card in full and want easier tracking or rewards.

Can online bill pay prevent late fees?

Yes, it can help if payments are scheduled early enough and the account has enough money.

Can bill pay payments fail?

Yes. Payments can fail due to insufficient funds, wrong payee details, processing delays, expired card details, closed accounts, or biller issues.

Are automatic payments always free?

Not always. Some billers or banks may charge fees depending on payment method. Always check terms.

How often should I review automatic payments?

Review automatic payments at least once a month. Also review after canceling subscriptions, changing cards, or switching banks.