International money transfers are now part of normal online banking.

People send money abroad for many reasons: supporting family, paying freelancers, receiving remote work income, paying suppliers, funding international tuition, booking travel, paying overseas invoices, moving savings, sending business payments, or managing money across countries.

But international transfers can be confusing.

One provider may advertise “no transfer fee” but use a weaker exchange rate. Another may show a transparent fee but give a better rate. A traditional bank may support SWIFT wires but charge higher fees. A digital transfer service may be cheaper but not available for every country or currency. A business account may offer batch payments and multi-currency tools, while a personal account may be enough for family remittances.

The best online bank or transfer provider for international payments should be clear about:

- Transfer fees

- Exchange rate markup

- Delivery time

- Supported countries

- Supported currencies

- Receiving method

- Transfer limits

- Bank account details

- SWIFT or local payment rails

- Business payment tools

- Security controls

- Refund and error process

- Regulatory protections

Wise says it uses the mid-market exchange rate and shows fees upfront. Revolut says international transfer costs can include real-time calculated transfer fees, possible flat fees for some SWIFT routes, and plan-based discounts. Bank of America says it does not charge a transfer fee for outbound international wires sent in foreign currency, but currency conversion markups are included in the exchange rate and other fees may apply.

That is why users should compare the total amount the recipient receives, not just the visible fee.

This guide compares the best online banks and digital providers for international transfers and global payments, explains how fees and exchange rates work, and gives practical safety tips before sending money abroad.

Important Disclaimer

This article is for general informational purposes only. It is not banking, legal, tax, investment, accounting, cybersecurity, remittance, or professional advice.

International transfer fees, exchange rates, delivery times, supported countries, transfer limits, account eligibility, compliance checks, refund rules, and provider availability can change. Always verify details directly with the bank, credit union, transfer company, or provider before sending money or opening an account.

What Is an International Bank Transfer?

An international bank transfer is a payment sent from one country to another.

It may be sent through:

- SWIFT wire transfer

- Local bank transfer network

- ACH-style payment rail

- SEPA transfer in Europe

- Faster Payments in the UK

- Card transfer

- Digital wallet transfer

- Remittance provider

- Multi-currency account

- Business payment platform

The recipient may receive money in:

- Local currency

- U.S. dollars

- Euros

- British pounds

- Another supported currency

International transfers can be sent by individuals or businesses.

What Are Global Payments?

Global payments are broader than personal money transfers.

They may include:

- Paying overseas suppliers

- Receiving remote work income

- Paying international contractors

- Sending marketplace payouts

- Paying tuition abroad

- Paying rent in another country

- Sending family remittances

- Receiving client payments

- Managing multi-currency business accounts

- Paying SaaS vendors

- Paying travel providers

- Moving funds between personal accounts in different countries

For freelancers, online businesses and remote workers, global payments can be essential.

Online Bank vs Money Transfer Provider

Many people use the phrase “online bank” for any digital money platform, but there are differences.

Online Bank

An online bank may offer:

- Checking account

- Savings account

- Debit card

- Online bill pay

- Wire transfers

- ACH transfers

- Mobile app

- FDIC or similar deposit coverage, depending on country

- Customer support

- Domestic and international transfer options

Examples:

- Capital One

- Bank of America online banking

- Chase online banking

- HSBC online banking

- SoFi

- Ally

- Revolut, depending on country and product structure

Money Transfer Provider

A money transfer provider specializes in sending money across borders.

Examples:

- Wise

- Remitly

- Western Union

- MoneyGram

- WorldRemit

- Xoom

- OFX

- Payoneer

They may offer:

- Lower transfer cost

- Local payment rails

- Better exchange-rate transparency

- Cash pickup, depending on provider

- Mobile wallet payout, depending on country

- Bank deposit

- Business payments

- Multi-currency accounts

Best Choice

For many users:

- Use an online bank for everyday banking.

- Use a specialist provider for international transfers.

- Use a business payment platform for freelancers and online businesses.

- Use a traditional bank wire for large regulated transfers or when required by recipient.

The best choice depends on where you send, how much you send, and how fast the money must arrive.

Best Online Banks and Providers for International Transfers

Below are strong options to compare. Availability, fees, countries, and features can change, so always verify current official details before sending.

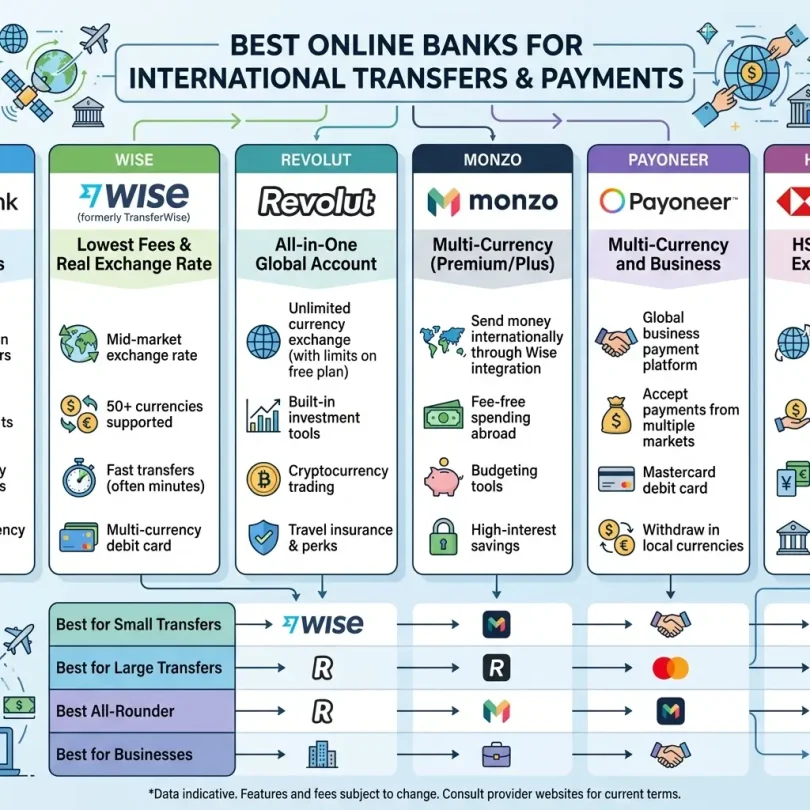

1. Wise

Best for: Transparent international transfers and multi-currency accounts

Good for: Freelancers, families, travelers, remote workers, small businesses

Main strength: Mid-market exchange rate and upfront fee display

Wise is one of the most popular international money transfer providers. It is known for transparent fees and mid-market exchange rates.

Wise says it uses the mid-market rate and shows fees upfront. Its pricing page states that it uses the mid-market rate and offers transparent fees, with lower prices for larger transfers through volume discounts.

Key Features

- International money transfers

- Mid-market exchange rate

- Transparent fees

- Multi-currency account

- Local account details in some currencies

- Debit card in supported regions

- Business account option

- Batch payments

- Payment links, depending on region

- Large country coverage

- App and website access

- Transfer tracking

- Rate comparison tools

Why Wise Is Good

Wise is strong because it makes the total cost easier to understand. Instead of focusing only on transfer fees, Wise shows the exchange rate and fee before you send.

This is useful because many international transfers hide cost inside exchange-rate markups.

Wise can also be useful for freelancers who receive money in multiple currencies and businesses paying overseas contractors.

Best Fit

Wise may fit:

- International freelancers

- Remote workers

- Families sending money abroad

- Small businesses

- Travelers

- Students abroad

- People who compare exchange rates

- Users needing multi-currency balances

- Businesses paying contractors

Possible Downsides

Wise may not support every country, every currency, or every payout method. Some transfers may require additional verification. Large transfers may take longer due to compliance checks.

2. Revolut

Best for: Multi-currency spending, transfers and travel-friendly banking

Good for: Travelers, remote workers, global users, app-first users

Main strength: Multi-currency app with global money movement tools

Revolut is a digital banking and money app available in many regions. It supports international transfers, multi-currency balances, card spending, and app-based money management.

Revolut says users can send money to accounts in more than 150 countries through bank transfers, send Revolut-to-Revolut payments quickly when both users have accounts, and send supported card transfers. Revolut also says transfer costs are shown before users commit.

Revolut’s broader website says it has more than 75 million customers globally and supports sending money to 160+ countries, holding up to 36 currencies in app, and spending in 150+ currencies.

Key Features

- International transfers

- Multi-currency account

- Revolut-to-Revolut transfers

- Card transfers, where available

- Bank transfers

- Currency exchange

- Debit card spending

- Travel-friendly tools

- Premium and Metal plan discounts, depending on region

- App-based account management

- Spending analytics

- Virtual cards

Why Revolut Is Good

Revolut is strong for users who travel, spend internationally, or manage multiple currencies from one app.

It is also useful when both sender and receiver use Revolut, because Revolut-to-Revolut transfers may be quick and have no transfer fee from Revolut, though currency exchange fees may apply.

Best Fit

Revolut may fit:

- Travelers

- Remote workers

- International students

- Digital nomads

- People sending to other Revolut users

- Users who hold multiple currencies

- App-first banking users

- People who want virtual cards

Possible Downsides

Fees, limits, and features vary by country and plan. Revolut also says intermediary banks may charge handling fees for some international SWIFT transfers, often outside Revolut’s control.

3. Bank of America Online Banking

Best for: Traditional bank international wires

Good for: U.S. users, large bank customers, wire transfer users

Main strength: Established bank wire transfer system

Bank of America allows customers to send domestic and international wire transfers through online banking or mobile banking.

Bank of America says it does not charge a transfer fee for outbound international wire transfers sent in foreign currency, but exchange rate markups apply, and recipient bank fees, foreign taxes, and other transfer process fees may apply.

Key Features

- International wire transfers

- Online and mobile wire setup

- Foreign currency wire option

- U.S. dollar international wire option

- Large bank support

- Recipient bank details

- Security verification

- Bank branch support

- Business banking options

- Wire history and receipts

Why Bank of America Is Good

Bank of America may be useful when the recipient requires a bank wire, when a traditional bank transfer is preferred, or when the sender wants a large bank relationship.

For some transactions, such as property payments, large business invoices, tuition payments, or formal overseas payments, traditional wires may still be requested.

Best Fit

Bank of America may fit:

- U.S. bank customers

- People sending formal wires

- Large transfer users

- Business customers

- People who prefer major banks

- Users needing branch support

- Customers already banking with Bank of America

Possible Downsides

Traditional wires may include exchange-rate markups and fees from intermediary or receiving banks. Users should compare the recipient amount with Wise, Revolut, OFX, and other providers before sending.

4. Chase Online Banking

Best for: U.S. customers needing bank-based international wires

Good for: Existing Chase customers, business users, large transfers

Main strength: Large bank wire system and branch support

Chase is one of the largest U.S. banks and supports online and mobile wire transfers for eligible customers.

Chase can be useful for customers who want traditional bank wire support, branch access, and a broad banking relationship.

Key Features

- International wire transfers

- Domestic wires

- Online banking

- Mobile banking

- Branch support

- Business banking

- Transfer receipts

- Security controls

- Recipient management

- Customer support

- Large bank infrastructure

Why Chase Is Good

Chase may be useful when you need a traditional wire and already bank with Chase.

It can also be helpful for small businesses that need international supplier payments, overseas invoices, or formal wire records.

Best Fit

Chase may fit:

- Existing Chase customers

- Small businesses

- Large transfer users

- Branch users

- People sending formal international wires

- Users who want a traditional bank

Possible Downsides

Bank wire transfers may cost more than specialist transfer providers after fees and exchange-rate markups. Always compare the final recipient amount.

5. HSBC Online Banking

Best for: International banking relationships

Good for: Expats, global families, cross-border account holders

Main strength: Global banking network

HSBC is known for international banking. It can be useful for people with accounts or relationships across countries.

HSBC may fit users who need bank accounts in multiple regions, global account management, and international banking services.

Key Features

- International bank network

- Cross-border banking

- Online banking

- Mobile banking

- International transfers

- Multi-country support, depending on region

- Foreign currency services

- Premier-style global account support, depending on eligibility

- Branch support in multiple markets

Why HSBC Is Good

HSBC can be useful for people who live, work, study, or do business across countries.

For expats and global families, having a bank with international presence can make account setup and transfers easier.

Best Fit

HSBC may fit:

- Expats

- International students

- Global families

- Cross-border workers

- Businesses with overseas activity

- People needing multi-country banking

- Users who value bank relationships

Possible Downsides

Fees and eligibility can vary widely by country and account type. Some HSBC products require higher balances or specific relationship status.

6. Capital One Online Banking

Best for: U.S. online banking users needing occasional international wires

Good for: Existing Capital One users, online banking users

Main strength: Digital banking with large-brand comfort

Capital One offers online and mobile banking, and some customers may use it for wire transfers and international banking needs depending on account type and availability.

Capital One can be useful for users who already use its checking or savings products and need occasional transfers.

Key Features

- Online banking

- Mobile banking

- Checking and savings

- Wire transfer support, depending on account

- Debit card

- Account alerts

- Large bank brand

- U.S.-based support

- Branch or café access in some regions

Why Capital One Is Good

Capital One may be a good fit for users who want one bank for domestic digital banking and occasional international transfers.

Best Fit

Capital One may fit:

- Existing Capital One customers

- U.S. online banking users

- Occasional international transfer users

- People who prefer large-brand banking

- Users who want checking and savings together

Possible Downsides

If you send money abroad frequently, a specialist provider may offer better transparency and total cost.

7. Payoneer

Best for: Freelancers and online businesses receiving global payments

Good for: Marketplace sellers, contractors, agencies, affiliate earners

Main strength: Receiving international business payments

Payoneer is widely used by freelancers, online sellers, agencies, and digital businesses that receive international payments from clients, platforms, and marketplaces.

It can be useful for people who receive money from platforms rather than simply sending family remittances.

Key Features

- Global receiving accounts

- Marketplace payment support

- Contractor payments

- Business payments

- Multi-currency balances

- Debit card options, depending on country

- Transfers to local bank

- Client payment requests

- Business dashboard

- Marketplace integrations

Why Payoneer Is Good

Payoneer is useful for freelancers and online businesses that receive payments from global platforms or international clients.

Examples:

- Freelance platforms

- E-commerce marketplaces

- Affiliate networks

- Client invoices

- Remote work payments

- Agency payments

Best Fit

Payoneer may fit:

- Freelancers

- Remote workers

- Marketplace sellers

- Agencies

- Affiliate marketers

- Online service providers

- International contractors

- Businesses receiving overseas payments

Possible Downsides

Fees can depend on how money is received, converted, and withdrawn. Users should compare fees carefully and check supported countries.

8. OFX

Best for: Larger international transfers

Good for: Property payments, business transfers, larger currency conversions

Main strength: Large transfer support and currency exchange focus

OFX is a specialist international money transfer provider often used for larger transfers.

It may be useful when sending bigger amounts for property, business payments, tuition, relocation, or supplier payments.

Key Features

- International money transfers

- Larger transfer support

- Currency exchange focus

- Personal and business accounts

- Transfer tracking

- Business payment tools

- Support for many currencies

- Phone support, depending on region

- Forward contracts and currency tools, depending on eligibility

Why OFX Is Good

OFX may be useful when transfer amount is larger and exchange rate matters more.

For large transfers, even a small exchange-rate difference can matter.

Best Fit

OFX may fit:

- Large transfer users

- Property buyers

- Overseas tuition payers

- Businesses paying suppliers

- People relocating

- Users comparing exchange rates

- Companies moving higher amounts

Possible Downsides

OFX may not be best for small urgent transfers. Some providers may be faster or easier for small family remittances.

9. Remitly

Best for: Family remittances and personal transfers

Good for: Sending money to family abroad

Main strength: Remittance-focused delivery options

Remitly is a remittance provider focused on sending money internationally to family and friends.

It may support bank deposit, cash pickup, mobile wallet, or home delivery depending on the receiving country.

Key Features

- International remittances

- Bank deposit

- Cash pickup, depending on country

- Mobile wallet, depending on country

- Delivery speed options

- Mobile app

- Transfer tracking

- Personal money transfers

- Country-specific payout methods

Why Remitly Is Good

Remitly can be useful for people sending money to family members who may not use the same bank or digital wallet.

It may be especially useful in countries where cash pickup or mobile wallet payout is common.

Best Fit

Remitly may fit:

- Family remittance senders

- Immigrants sending money home

- People sending small or medium amounts

- Users needing cash pickup options

- People sending to countries with mobile wallet support

Possible Downsides

Compare exchange rates and fees carefully. Delivery speed and cost may vary by payment method and receiving country.

10. Western Union Digital

Best for: Wide global payout network

Good for: Cash pickup, remote locations, family remittances

Main strength: Large physical and digital network

Western Union is one of the most recognized money transfer brands. It offers digital transfers and cash pickup options in many countries.

Key Features

- International money transfers

- Digital sending options

- Cash pickup

- Bank deposit

- Mobile wallet in some regions

- Large agent network

- Transfer tracking

- Personal remittance support

- Multiple payout options

Why Western Union Is Good

Western Union can be useful when the recipient needs cash pickup or is in a location where bank access is limited.

It may be less about low cost and more about reach and payout flexibility.

Best Fit

Western Union may fit:

- Family remittances

- Cash pickup users

- Recipients without bank accounts

- Remote location transfers

- Urgent personal transfers

- Users needing physical pickup options

Possible Downsides

Fees and exchange rates may be less favorable than some digital-first providers. Always compare recipient amount before sending.

Quick Comparison Table

| Provider | Best For | Main Strength | Best User Type |

|---|---|---|---|

| Wise | Transparent transfers | Mid-market rate and upfront fee | Freelancers, families, businesses |

| Revolut | Multi-currency app | Spending and transfers in many currencies | Travelers and remote workers |

| Bank of America | Traditional wires | Large bank wire system | Existing bank customers |

| Chase | Bank-based wires | Branch and wire support | U.S. business users |

| HSBC | Cross-border banking | Global bank network | Expats and global families |

| Capital One | Occasional wires | Digital banking with large brand | U.S. online banking users |

| Payoneer | Receiving global payments | Marketplace and client payments | Freelancers and sellers |

| OFX | Large transfers | Currency-focused transfers | Large transfer users |

| Remitly | Family remittances | Country payout options | Family senders |

| Western Union | Cash pickup | Wide payout network | Recipients needing cash |

How International Transfer Fees Work

International transfers may include several cost layers.

1. Transfer Fee

This is the visible fee charged by the provider.

It may be:

- Flat fee

- Percentage fee

- Real-time calculated fee

- Card funding fee

- Wire fee

- Same-day transfer fee

2. Exchange Rate Markup

This is often the hidden cost.

If the market rate is 1 USD = 280 PKR, but the provider gives 1 USD = 274 PKR, the difference is a markup.

A provider can advertise “no fee” but still make money through the exchange rate.

3. Intermediary Bank Fee

For SWIFT transfers, intermediary banks may deduct fees before the money arrives.

Revolut notes that for international SWIFT transfers, external and intermediary banks may charge handling fees.

4. Receiving Bank Fee

The recipient’s bank may charge an incoming wire fee.

5. Card Funding Fee

If you pay with a debit or credit card, fees may be higher.

6. Cash Pickup Fee

Cash pickup transfers may cost more than bank deposits.

7. Plan-Based Fees

Some providers offer cheaper transfers on paid plans.

Revolut says Premium or Metal users may receive discounts or no-fee transfers included in the plan, depending on terms.

Exchange Rate: The Most Important Thing to Compare

Do not compare transfer fee only.

Always compare:

- Amount you send

- Transfer fee

- Exchange rate

- Recipient receives

- Delivery time

- Any receiving fees

The most important number is:

Recipient gets

Wise offers a comparison tool showing providers, exchange rates, fees, and final recipient amount for a sample transfer.

Example

Provider A:

- Fee: $0

- Weak exchange rate

- Recipient gets less

Provider B:

- Fee: $5

- Better exchange rate

- Recipient gets more

Provider B may be cheaper even though it charges a visible fee.

SWIFT Wire vs Local Transfer Network

SWIFT Wire

SWIFT is a global messaging network used by banks for international wires.

Good for:

- Large transfers

- Formal bank transfers

- Business payments

- Tuition payments

- Property payments

- Countries with limited local payment options

Possible downsides:

- Higher cost

- Intermediary bank fees

- Slower delivery

- More bank details required

- Less predictable recipient amount

Local Transfer Network

Some providers use local bank rails.

Example:

- Sender pays Wise locally in one country

- Recipient receives local bank transfer in another country

Good for:

- Lower cost

- Faster delivery

- Better fee visibility

- Smaller transfers

- Family remittances

- Freelancer payments

Possible downsides:

- Not available in every corridor

- Transfer limits

- Provider verification

- Country restrictions

Best Provider by Use Case

Best for Family Remittances

Compare:

- Wise

- Remitly

- Western Union

- Revolut

- Xoom

Focus on:

- Recipient receives amount

- Delivery method

- Cash pickup

- Mobile wallet

- Bank deposit

- Speed

- Support

Best for Freelancers

Compare:

- Wise

- Payoneer

- Revolut

- OFX

- Local bank wire

Focus on:

- Receiving account details

- Client payment ease

- Multi-currency balances

- Withdrawal fees

- Exchange rate

- Business records

Best for Small Businesses

Compare:

- Wise Business

- Payoneer

- OFX

- Mercury, where relevant

- Bank wire through Chase or Bank of America

- HSBC business banking

Focus on:

- Supplier payments

- Batch payments

- Invoice payments

- Currency conversion

- User permissions

- Accounting exports

- Business verification

Best for Travelers

Compare:

- Revolut

- Wise

- Capital One

- HSBC

- Local bank debit cards

Focus on:

- Foreign card spending fees

- ATM fees

- Currency exchange

- Multi-currency balance

- App controls

- Virtual cards

Best for Large Transfers

Compare:

- OFX

- Wise

- Bank wire

- HSBC

- Bank of America

- Chase

Focus on:

- Exchange rate

- Transfer limits

- Compliance checks

- Bank requirements

- Support

- Receipt documentation

Best for Cash Pickup

Compare:

- Western Union

- Remitly

- MoneyGram

- WorldRemit

Focus on:

- Pickup locations

- Recipient ID requirements

- Fee

- Exchange rate

- Pickup hours

- Customer support

International Transfer Safety Tips

1. Verify Recipient Details

Check:

- Full name

- Bank name

- Account number

- IBAN

- SWIFT/BIC

- Routing number

- Recipient address

- Country

- Currency

A wrong detail can delay or misdirect money.

2. Send a Small Test Transfer

For new recipients, send a small test amount first.

This is useful for:

- Large transfers

- New supplier payments

- New contractor payments

- New bank accounts

- Tuition payments

- Property payments

3. Beware of Urgent Transfer Scams

Scammers may pressure you to send money quickly.

Common scams:

- Fake family emergency

- Fake romance partner

- Fake investment platform

- Fake bank call

- Fake tech support

- Fake immigration problem

- Fake government fine

- Fake job offer

- Fake rental listing

- Fake supplier invoice

Stop and verify before sending.

4. Do Not Send Money to Unknown People

Do not send international transfers to people you only know online unless fully verified.

5. Use Official Websites and Apps

Download apps only from official app stores.

Do not click transfer links from random emails, messages, or social media.

6. Compare Recipient Amount

Before sending, compare the final amount the recipient gets across providers.

7. Save Receipts

Keep:

- Transfer confirmation

- Receipt number

- Exchange rate

- Fee

- Recipient details

- Delivery estimate

- Support contact

- Bank statement

8. Know Your Rights

The CFPB says certain federal protections apply when consumers in the U.S. send more than $15 to a person or company in another country through a qualifying remittance transfer provider.

These protections may include disclosures and error-resolution rights, depending on the transfer type and provider.

9. Avoid Public Wi-Fi

Do not send money using public Wi-Fi.

10. Turn On Account Alerts

Use alerts for:

- Login

- Transfer created

- Transfer completed

- Password change

- New device

- Bank account added

- Large transfer

- Failed transfer

Common International Transfer Mistakes

Mistake 1: Comparing Only Fees

A $0 fee transfer can still cost more if the exchange rate is poor.

Mistake 2: Ignoring Intermediary Bank Fees

SWIFT transfers may lose money along the route.

Mistake 3: Sending the Wrong Currency

Sometimes sending foreign currency is better. Sometimes sending USD is better. Compare both.

Mistake 4: Not Checking Recipient Bank Rules

Some banks reject transfers if details are incomplete.

Mistake 5: Sending Large Amount Without Testing

Always test a small transfer when possible.

Mistake 6: Trusting Fake Transfer Apps

Use official app stores and verified websites.

Mistake 7: Falling for Emergency Scams

Urgency is a warning sign.

Mistake 8: Not Saving Receipts

Receipts matter if a transfer is delayed or disputed.

Mistake 9: Ignoring Transfer Limits

Limits can delay business payments or tuition transfers.

Mistake 10: Not Checking Local Rules

Some countries have restrictions, reporting rules, or compliance checks.

International Transfer Checklist

Before sending money abroad, check:

- Is the provider available in my country?

- Is the recipient country supported?

- Is the receiving currency supported?

- What is the transfer fee?

- What is the exchange rate?

- How much will recipient receive?

- Are there intermediary bank fees?

- Are there receiving bank fees?

- How long will transfer take?

- What payment method is cheapest?

- What payment method is fastest?

- Is cash pickup needed?

- Is bank deposit available?

- Is mobile wallet payout available?

- Are there transfer limits?

- Is identity verification required?

- What documents are needed?

- Can I track the transfer?

- What happens if details are wrong?

- What are refund rules?

- What support is available?

Best Setup for Different Users

Family Sender Setup

Use:

- Wise for transparent bank deposit

- Remitly for remittance corridors

- Western Union for cash pickup

- Revolut if both users have accounts

Freelancer Setup

Use:

- Wise for multi-currency receiving

- Payoneer for marketplace payments

- Revolut for multi-currency spending

- Local bank for domestic withdrawal

Small Business Setup

Use:

- Wise Business for supplier payments

- Payoneer for marketplace/client payments

- OFX for larger transfers

- Traditional bank wire for formal payments

- Accounting exports for records

Traveler Setup

Use:

- Revolut

- Wise card, where available

- Low foreign-fee bank card

- Backup bank account

- Travel alerts

Large Transfer Setup

Use:

- OFX

- Wise

- Bank wire

- HSBC

- Bank of America or Chase

Always compare exchange rate, recipient amount, and documentation requirements.

Final Verdict: What Are the Best Online Banks for International Transfers?

The best online bank or provider for international transfers depends on your use case.

For most users:

- Best transparent international transfers: Wise

- Best multi-currency app: Revolut

- Best traditional U.S. bank wire option: Bank of America

- Best large U.S. bank wire alternative: Chase

- Best global banking relationship: HSBC

- Best occasional large-brand online banking option: Capital One

- Best for freelancers receiving global payments: Payoneer

- Best for large international transfers: OFX

- Best for family remittances: Remitly

- Best for cash pickup network: Western Union

If you send money abroad often, Wise and Revolut are worth comparing first because they show fees clearly and focus on cross-border movement. If you receive international freelance or marketplace income, compare Wise and Payoneer. If you need large formal wires, compare OFX, HSBC, Bank of America, and Chase. If your recipient needs cash pickup, compare Remitly and Western Union.

The best provider is not always the one that says “no fee.” The best provider is the one that gives the recipient the most money safely, quickly, and transparently.

FAQs About Online Banks for International Transfers

What is the best online bank for international transfers?

Wise is strong for transparent international transfers, Revolut is useful for multi-currency app users, HSBC is good for global banking relationships, and traditional banks like Bank of America or Chase can work for formal wires.

Is Wise good for international transfers?

Yes. Wise is popular because it uses the mid-market exchange rate and shows fees upfront.

Is Revolut good for international transfers?

Revolut can be useful for multi-currency transfers and travel users. It says users can send money to accounts in more than 150 countries and see costs before confirming.

Are bank wires cheaper than Wise?

Not always. Bank wires may have transfer fees, exchange-rate markups, intermediary bank fees, and receiving bank fees. Compare the final recipient amount.

What is SWIFT?

SWIFT is a global messaging network used by banks for international wire transfers. It is commonly used for formal bank-to-bank international payments.

What is the cheapest way to send money internationally?

The cheapest method depends on country, currency, payment method, amount, and provider. Compare Wise, Revolut, Remitly, OFX, and your bank before sending.

Why do “no fee” transfers still cost money?

A provider may charge no visible transfer fee but use a weaker exchange rate. The hidden cost is in the exchange-rate markup.

What is the mid-market exchange rate?

The mid-market rate is the rate between buy and sell prices in currency markets. Wise says it uses the mid-market rate for conversions.

Are international money transfers protected?

In the U.S., certain protections apply for qualifying remittance transfers over $15 sent to a person or company in another country.

Can international transfers be reversed?

Sometimes, but not always. It depends on provider, transfer status, recipient bank, country, and rules. Contact the provider immediately if there is a mistake.

Which provider is best for freelancers?

Wise and Payoneer are strong options for freelancers. Wise is useful for multi-currency transfers and Payoneer is useful for marketplace and client payments.

Which provider is best for cash pickup?

Western Union and Remitly are commonly compared for cash pickup, depending on receiving country and available locations.